The government’s initial response to the petition to make financial education in schools compulsory is that it isn’t really necessary. All that is needed, claims the government, is to encourage parents to teach their kids, and to tweak an existing non-compulsory “Personal, Social, Health, and Economic” school course about which I will come back to below.

Once again, our rulers see their prime responsibility as helping the companies help themselves. Successive governments have ensured weak laws, puny regulators, and now they would withhold education from children. After all, consumer law puts the responsibility of being "reasonably well informed" on the consumer. Keeping customers ignorant is a loophole in consumer law that bankers riding camels can canter through.

Times have changed so little, with the mass of the population regarded by our supposed guardians as lawful prey. Presumably they see themselves not as shepherds, but as game-keepers.

The British ruling classes once had a simple formula when it came to their children. Knowing they needed a male heir and a couple of spares (in case of accidents) to ensure the inherited lands and chattels stayed in the family, they bred at least a brace and a half of sons. To keep the boys gainfully employed they plotted their career paths thus:

- The oldest inherited

- The second joined the army

- The third became a priest

Not only did this keep the purse strings in family hands, it also kept those strings tied firmly as a garrotte around the neck of the nation. In churches around the country congregations once enthusiastically sang:

All creatures great and small,

All things wise and wonderful,

The Lord God made them all.

The rich man in his castle,

The poor man at his gate,

God made them high and lowly,

And ordered their estate.

To keep the poor at the first son’s gate, the third son would tell the population that god willed it so, and the second son threatened to thump them if they dared touch the railings.

Times change. Inheritance no longer goes automatically to the oldest male – not even the British crown. The priesthood and the army are no longer careers of choice among the wealthy. And that “rich man in his castle” verse has disappeared from the hymn in many modern hymnals.

However, “plus ça change, plus c’est la même chose”, the more things change the more they stay the same. From the way we Britons continue to be ripped off, it seems that the new mercantile gentry now dispose of their children thus:

- The oldest becomes a banker

- The second a regulator

- The third a judge

- The illegitimates become MPs

Land is not the cash-cow it once was - the cash-cow is now us ripped-off Britons. How else can we explain the series of ‘great escapes’ the financial services industry has pulled off? All passed with a cheery wave by the regulators and the courts: excessive overdraft charges; pillaging with-profits fund assets; excessive pension charges; the rip-off of teaser rates. Scams costing ripped-off Britons literally £billions that regulators, judges, and parliament have decreed to be just fine.

The illegitimates in parliament have given their initial response to the petition to make Financial Education compulsory in schools, which successfully reached its target 100,000 signatures. Reaching this target means the government must consider debating it in Parliament. The government asserts that this task can be taken on by parents helping out their kids, plus tweaking the PSHE curriculum a bit.

They claim that “Parents can also play a crucial role in helping young people to become financially aware..” Really? Repeated corporate shenanigans have shown that companies from banks to telecoms to energy to supermarkets find bamboozling their adult customers a very easy challenge. One reason parents are so easily ripped off is because there was no compulsory financial education during their school days.

So let’s take a closer look at the government’s other assertion that improving the quality of “Personal, Social, Health and Economic (PSHE) education” will prepare the children for the world of finance. We assume, being the optimists we are, that the government’s idea of preparation doesn’t involve laying the sucklings on a silver tray with an apple in their mouths and sprigs of parsley between their toes. So what is PSHE is all about?

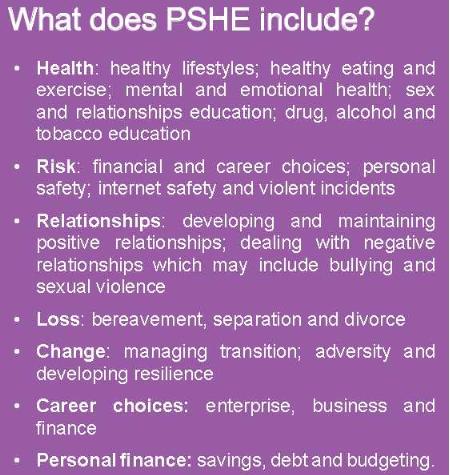

According to the PSHE Association, this course is intended “to help learners develop the knowledge, understanding and skills they need to manage their lives, now and in the future”. It covers topics that are of a far more immediate danger to children – drugs, nutrition, pregnancy, communicable diseases, crime – than bankers. The PSHE Association’s leaflet provides this description of "What does PSHE include?"

According to the PSHE Association, this course is intended “to help learners develop the knowledge, understanding and skills they need to manage their lives, now and in the future”. It covers topics that are of a far more immediate danger to children – drugs, nutrition, pregnancy, communicable diseases, crime – than bankers. The PSHE Association’s leaflet provides this description of "What does PSHE include?"

At a more academic level, the course of study by AQA, one of the main school examining boards in the UK, Section 9.6 states:

"Knowledge and appreciation of the need to develop skills associated with spending money, i.e. essential and non-essential spending, ways of budgeting, the use of hire purchase, direct debit, credit and debit cards, internet banking etc. The importance of money management, earning, spending, saving and the various forms of borrowing. The need for financial planning for the future, particularly pensions and investments. How to access financial guidance."

Which all sounds pretty good. But to crystallise what is taught and to what level, one has to look at the exam papers. Typically there was just one question about using financial services. In 2009 it was:

The examining board’s answer sheet for this question states:

As can be seen from this question and answer the ‘economic’ part of PSHE teaches children what financial services to use, which is a good thing. However, it does not teach how the Financial Services abuse their clients. It is like the government encouraging children to learn to swim by telling them where the sea is, but refusing to tell them that it is totally infested with sharks and the chances of them losing a limb are almost certain.

Financial education in schools must not be about what financial products can be bought – youths and adults are constantly bombarded with advertising about this through their lives. Financial education in schools should be about understanding the traps.

An examination for Financial Education in Schools should have questions like these:

ANSWER - 92% of your income is lost.

- 0.5% ANSWER - 18%

- 1.0% ANSWER - 33%

- 1.5% ANSWER - 45%

- 2.0% ANSWER - 55%

ANSWER - 29 years (bonus mark for stating this is 10 years after the average person is dead)

The correct place for this financial education is as part of the Maths curriculum. You don’t need a highly paid consultant to work this out. Sit a few maths teachers down with cups of tea and slices of cake, and they will tell you there are enough topics in the current GCSE (the exam children take at 16 years of age) that can be dropped and others that can be delayed into A-Level to make space for a financial module.

- Constructing a perpendicular from a point to a straight line may have grabbed the admirers of Pythagoras, but I ask you, when was the last time you had to do that in your adult life (other than doing your child’s homework)?

- Factorising quadratics may be useful to scientists, engineers, and academics, but it is a skill that won’t be missed by herds of well paid professionals who do not do maths beyond GCSE.

Creating space in the existing maths curriculum for financial education would be easy, would be relevant to the subject, and would build financial skills to make our young Britons less ripped-off.

Of course Financial Education in schools won’t solve everything. One of the most efficient ways of ripping off someone’s money is to not give it to them in the first place. To pull this one off, you need to be in a position of power or trust so you can abuse it. Typically this would be an employer, keeping pay down for all except friends and family, or a financial institution as custodian of the nation’s savings. Weaselly little scams like paying pitiful interest rates to savers afflict even the more sophisticated investors. For instance, people who invest their pensions themselves in SIPPs (Self Invested Personal Pensions).

There must be a lot of vertebrae littering the offices of the FSA. It would be unfair to say they were a spineless bunch. More accurate to say that their spinal chords are routinely pulled out. In February 2011 someone in the FSA showed enough spine to state:

“Making and retaining a secret profit from the customer’s money” – strong words! It was bravely proposed by this courageous regulator that “there should be clear disclosure of the fact that interest is retained and the amount”.

It is a sign of our ripped-off times that this is not obviously the right thing to do. How the building must have echoed with the clatter of vertebrae hitting the marble floors at the FSA offices in Canary Wharf last week. The FT reported that the FSA backed down when it published its final decision on 8th November, which had no sign of this requirement. Doing a document word search for “interest” finds just three instances all of which use it in the context “not boring”, none of which relate to secretly profiting from the customer’s money. According to the FT, the Association of British Investors claimed this would have “created significant practical and commercial issues” for the providers. Which presumably means:

- Practical issue: How do we tell our customers we are secretly pocketing their investment income?

- Commercial issue: How do we pay our bonuses if we don’t secretly pocket our customers’ investment income?

Why the banks and insurers do this kind of thing, and why the authorities allow them to get away with it, is not a subject for Financial Education in schools. More suited to the Religious Education class: if there is a god, and that god is benevolent, then why the devil does that god allow the world to be such a vale of rip-offs that impoverish us Britons?

Governments borrow billions. To try and keep the costs down, they borrow money for different lengths of time, typically between 3 months and 30 years, so they can negotiate better terms with different types of investors. This means they have to continually re-finance their debt. As one loan becomes due, they borrow another chunk of money to pay it off. The Economist newspaper shows the gory details: figures for France, Italy and Spain show they need to borrow fresh € billions each week not to fund fresh spending but just to pay back their existing loans.

Governments borrow billions. To try and keep the costs down, they borrow money for different lengths of time, typically between 3 months and 30 years, so they can negotiate better terms with different types of investors. This means they have to continually re-finance their debt. As one loan becomes due, they borrow another chunk of money to pay it off. The Economist newspaper shows the gory details: figures for France, Italy and Spain show they need to borrow fresh € billions each week not to fund fresh spending but just to pay back their existing loans.

Neither the previous Labour nor the current Conservative led government wanted to waste a good crisis: both eagerly took the opportunity to reduce the circumstances of us ripped-off Britons by cutting salaries, pensions, benefits, and laying people off. Proposals have been made to water down the minimum wage and allow employers to dismiss staff without a reason. Borrow more, or cut benefits and sack the less well off. The repeated lie that "we are all in this together". Both political parties chose to ignore the third option staring us in the face. The third way may not be a pretty option, but in this crisis none of them are. The third way, whisper it softly, a well targeted tax aimed at the best kept open secret tax haven.

Neither the previous Labour nor the current Conservative led government wanted to waste a good crisis: both eagerly took the opportunity to reduce the circumstances of us ripped-off Britons by cutting salaries, pensions, benefits, and laying people off. Proposals have been made to water down the minimum wage and allow employers to dismiss staff without a reason. Borrow more, or cut benefits and sack the less well off. The repeated lie that "we are all in this together". Both political parties chose to ignore the third option staring us in the face. The third way may not be a pretty option, but in this crisis none of them are. The third way, whisper it softly, a well targeted tax aimed at the best kept open secret tax haven.

In real terms, the wealth concentrated in the pockets of the wealthy has grown healthily. Even the 2008 dip in asset prices leaves asset prices well above historical levels in real terms. In France they already have a separate wealth tax they call "L'impôt de solidarité sur la fortune", the solidarity tax by which the wealthy show their solidarity with everyone else.

In real terms, the wealth concentrated in the pockets of the wealthy has grown healthily. Even the 2008 dip in asset prices leaves asset prices well above historical levels in real terms. In France they already have a separate wealth tax they call "L'impôt de solidarité sur la fortune", the solidarity tax by which the wealthy show their solidarity with everyone else.

According to the PSHE Association, this course is intended “to help learners develop the knowledge, understanding and skills they need to manage their lives, now and in the future”. It covers topics that are of a far more immediate danger to children – drugs, nutrition, pregnancy, communicable diseases, crime – than bankers. The PSHE Association’s leaflet provides this description of "What does PSHE include?"

According to the PSHE Association, this course is intended “to help learners develop the knowledge, understanding and skills they need to manage their lives, now and in the future”. It covers topics that are of a far more immediate danger to children – drugs, nutrition, pregnancy, communicable diseases, crime – than bankers. The PSHE Association’s leaflet provides this description of "What does PSHE include?"

{kind=link}