The government and the pension industry are continually preaching to us that we are saving too little. They deploy vast advertising and advisory budgets to get this particular gospel across to us. You’ll be doomed if you don’t save, they tell us, but there is a nagging suspicion that we will be doomed if we do save too.

It would be unfair to say government and pension fund managers are entirely in cahoots. Each have their own separate reasoning for their common cause:

a) The government, so it can transfer the blame for pensioner poverty to the pensioners, for not saving enough. A low cost and curt “I did warn you!” is much cheaper than actually doing something about it. It’s a tactic from the same handbook as putting “Smoking Kills” on packets of cigarettes – nothing to do with warning the smoker, everything to do with providing an “I told you so” defence in compensation court.

b) The pension industry so it can rip us off. The impact of pension fund charges, which typically range between 0.5% and 5%, can slash your savings by over 50%. For a prudent young person planning for the future thus;

- 25 years old, planning to contribute for 40 years until they are 65

- £100 per month, increasing by 3% each year

- Fund growing at 6% per year

A report by the RSA (Royal Society for the encouragement of Arts, Manufactures and Commerce) found that a reasonable charge would be 0.5%, and that excessive charges in the UK meant:

Let’s put the government to one side and focus on the pensions industry, for now. The government will wait for another time. You need a bit of mathematics to explain what is possibly the widest reaching, most chronic, and most ruthless rip-off of them all. To be more precise, widest reaching, most chronic, and most ruthless sequence of rip-offs. “Sequence”, because you are ripped off during every stage of your life.

STEP 1. As a worker: to get the tax benefits you are required to save for your pension with ‘regulated’ providers. If you take all the money you save, plus the returns on the investment, over a working life of 40 years, you will find the provider takes up to half of it in charges.

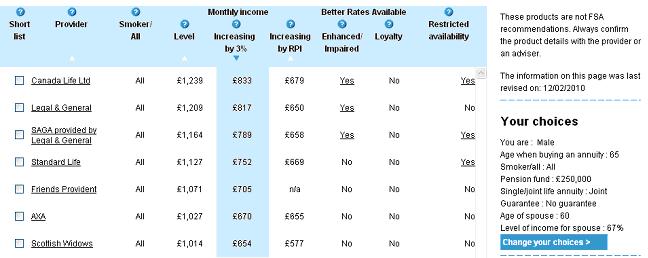

STEP 2. On retirement: or by the time you are 77, you are required to buy an annuity. You take all the money you saved during your life, and you give it to a pension company. In return they will give you an annual amount which will be as paltry as they can get away with. The pension company will, by default, give you a terrible return. They will try to bamboozle you with ‘future proofed’ pensions that grow with time. Omitting to tell you that 'future proofing' means you start with about a third less monthly income, and it will probably take a couple of decades to catch up with amount you would have got with a non-future-proofed pension. The maths, which I will explain in a future post, shows that if you take your future-proofed pension at 65 you could be over 90 before you see any extra cash.

STEP 3. On passing away: Having retired and bought an annuity, when you die your pension stops and your pension fund is taken by the provider. If you invested £500,000 with them, and you lived for 1 day or for 10 years drawing at a rate of £25,000 a year – then when you die, the remaining money becomes the property of the pension provider.

STEP 0 (this rip-off is cyclical). As a child: the wealth your parents built up for their retirement, their savings built up by skimping on your holidays, sweeties, birthday presents, and private education, is grabbed when they pass away. Not a farthing of the money they used to buy the annuity for their old age will you find in the inheritance carve-up.

For this week, I will concentrate on STEP 1, the charges, leaving STEP 2, 3 and 0 for future weeks. Fund management is perhaps one of the greatest financial rip-offs in current times. If the government is actually serious about reining in bankers’ bumper bonuses, they don’t need to put caps on remuneration. They simply need to control the contribution rip-offs make to bank profits – deflating that particular balloon would go a long way to bringing the bonuses down to earth.

Investment funds in the UK typically charge anything between 0.5% and 5% per annum to provide their service. At first it doesn’t sound so much. After all, at a restaurant you would typically leave a 10% service charge for the waiter. But the investment fund takes their service charge every year. It’s as if the waiter is sitting at the table with you eating your lunch. In the world of pension funds, you pay for your meal during the meal, but only get to eat your share once the waiter has finished – that is to say when you retire and get your pension payments.

For those who do invest in pension and other funds, taking a closer look at the mathematics of a mid-level 2% per annum investment fund charge reveals the catastrophic impact of the charge on a 40 year investment. The maths also reveals a further well hidden cost of the charges, on top of the charges themselves:

- You earn interest on the amount you have invested.

- When you pay a charge, the amount you have invested is reduced.

- Therefore the cost to you is not only the accumulated charges, but also the lost investment income that would have accrued had those charges not been made.

- Effectively, the money you are charged has moved to someone else’s account and is earning them interest instead of you.

To keep things simple, here is an illustration if you made a single £1,000 investment and made no further contributions.

After 40 years, earning 6% and paying a charge of 2% per annum, the £1,000 is worth £4,584 and the accumulated charges over this period have been £1,848. However, the removal of the £1,848 over the 40 years has also resulted in a loss of a further £3,854 in investment income if you had kept that £1,848. So the total cost to you is £1,848 + £3,854 = £5,702 – more than halving what your investment would have been worth without any charges.

Could it be that the fund manager is worth the cost of his hire? There is an ongoing debate around whether passive Index Tracking funds can be beaten by actively managed funds in which ‘clever’, i.e. highly paid, fund managers duck and dive between stocks and cash striving to win extra profits. However the overall statistics show that over a period of 5 years, Index Tracking beats the great majority of actively managed funds. Standard & Poor’s (S&P), a financial research company, produces a quarterly report the S&P Indices versus Active Funds Scorecard (SPIVA). The SPIVA report for North American funds in the year 2008 stated

- Over the five year market cycle from 2004 to 2008, the S&P 500 index outperformed 71.9% of actively managed large cap funds, S&P MidCap 400 outperformed 79.1% of mid cap funds and S&P SmallCap 600 outperformed 85.5% of small cap funds. These results are similar to that of the previous five year cycle from 1999 to 2003.

- The belief that bear markets favor active management is a myth. A majority of active funds in eight of the nine domestic equity style boxes were outperformed by indices in the negative markets of 2008. The bear market of 2000 to 2002 showed similar outcomes.

- Benchmark indices outperformed a majority of actively managed fixed income funds in all categories over a five-year horizon. Five year benchmark shortfall ranges from 2-3% per annum for municipal bond funds to 1-5% per annum for investment grade bond funds.

- The script was similar for non-U.S. equity funds, with indices outperforming a majority of actively managed non-U.S. equity funds over the past five years

The Financial Services Authority provides comparison tables, including tables for pension providers. The charges that our prudent 25 year old saving £100 per month and planning to retire at 65 range from £40,000 to £124,000 depending on the rapaciousness of the fund manager's fee. The Financial Times market data service lets you see the performance of one of the most expensive providers on the list compared to the FTSE All Share Index:

Over the last 10 years the FTSE Index has matched or outperformed the expensive fund’s own index tracker as well as its actively managed fund.

All the talk by government and the pensions industry about Ripped-off Britons working longer and living leaner is missing one big point. By stopping the fund managers ripping out 50% of the value of pension funds, you can at a stroke make a giant stride towards dealing with the pension crisis. And also make a giant stride towards dealing with excessive pay in the financial services industry.