Guest post by a banking insider at www.honestlybanking.co.uk

Are you being Churned over? Would you even know if you were?

Many investors have not heard of ‘Portfolio Turnover’ but it's much loved by stockbrokers, fund managers and bankers as it provides a nice way to increase their income without you noticing and without them having to tell you.

Portfolio Turnover is the frequency with which assets within a portfolio are bought and sold. Given that it costs you each time there’s a trade (trading commission plus stamp duty) and it has a big impact on your overall return, you should pay close attention to it. The manager of your money will always find a good reason to buy or sell an asset. They can always find a justification to sell a particular share or fund, this helps them avoid any allegations of wrongdoing. But each time its done, they collect a bit more commission and earn bigger bonuses.

When trading becomes excessive it is called churning or overtrading and is unlawful. Additionally the Annual Management Charge (AMC) and the Total Expense Ratio (TER) do not include the costs incurred to you by Portfolio Turnover. These extra costs that are racked up include commissions, stamp duty and the bid/offer spread.

The Financial Times[1] states that some funds annual turnover rate can be 500%. The average in the UK is 89%. This adds about 0.9% in addition to the quoted TER (Total Expense Ratio). If you’re already paying 1% for management this is nearly doubling the cost of the investment. In reality you are likely to be paying far more than this, but even this extra 0.9% is going to have a major impact on your money over time.

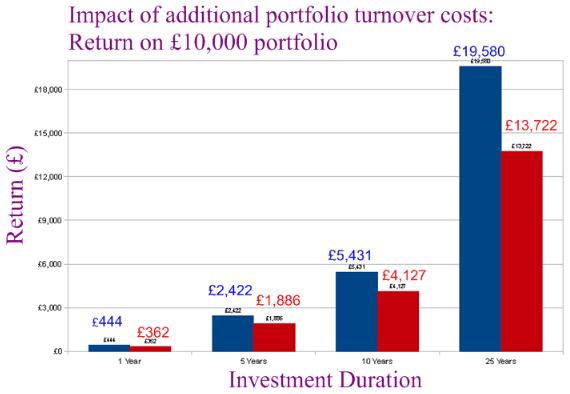

This chart shows the actual difference in return based on a £10,000 investment over periods of time and the impact of the costs of a higher portfolio turnover. The Blue represents a TER (Total Expense Ratio) of 1.5% and the red a TER of 2.4% (add additional 0.9% of costs from higher portfolio turnover). Even in one year you are 20% worse off with a higher portfolio turnover. The gross returns are the same, but the additional cost has a huge and compounding impact on your net return over time.

It used to be easier to find out about Portfolio Turnover, but a new piece of financial legislation (with the snappy name of UCITS IV removed the requirement to report Portfolio Turnover in July 2011. The reasoning behind this was that it was too complicated for investors to understand, though financial products in the USA and Australia manage to report it sensibly enough. It’s rather ironic as this legislation was supposed to encourage competition in investments across the EU and provide standardised information so that investors can make more informed choices. Instead the industry is hiding a key statistic.

The IMA (Investment Management Association) is the trade association and lobby group for the investment industry. Their Senior Advisor Mark Sherwin[2] says that:

“Existing Portfolio Turnover figures are open to misinterpretation, as they include times when the fund manager is forced to buy or sell shares because of inflows and outflows of money into an open-ended fund”

In other words the IMA thinks investors are too stupid to understand why a fund buys or sells assets, or maybe there’s another reason why they lobbied to have it removed?

The IMA’s present position seems to contradict its own guidance[3] in which it says about Portfolio Turnover:

“This figure enables comparisons with other funds and gives an indication of the possible impact of such transactions on fund performance”

Of course the Portfolio Turnover is an issue that the Fund Manager or Stockbroker might not want to talk about, but if there’s good reason for it, why not be open?

The excessive buying or selling of assets, or churning, is unlawful in most other jurisdictions as well. It does go on and here at Honestly Banking we have heard of many cases whereby stockbrokers have been pressured to increase revenue by driving up commissions through increasing Portfolio Turnover. This is particularly prevalent at critical times, such as before the end of the financial, quarter, year, or when bonus when payments are being decided.

The highly regarded Fund Manager, Neil Woodford[4], reports that the average stock holding period has dropped from over 5 years to 7.5 months over the last 40 years. There may be other reasons for this, but increasing Portfolio Turnover is a worrying trend. Of course when funds are performing well the costs tend to get glossed over.

The legendary Warren Buffet has a very different view on Portfolio Turnover and says that he likes to buy a stock that he would still be happy to hold even if the stock market was closed for 10 years. It’s not surprising that his renowned fund has a Portfolio Turnover rate of 10%. Buffet takes a long term view and likes to buy and keep his holdings. He also adds that he makes most money when he is snoozing rather than actively trading!

High levels of Portfolio Turnover can also be used to make up for lower management charges. Again we know of one well known charity who were pleased to have negotiated a low Annual Management Charge (AMC) but the broker they used went on to turnover the portfolio at a higher than usual level to help make up this revenue. Of course the broker could always find good justifications for doing so, particularly early on when they used the excuse of ‘sorting out inherited problems with the portfolio’ as the reason for at least 2 years.

Of course it’s easier to churn within a fund as most investors take little notice of changes in the funds constituents and often the standard reporting normally only shows the top ten holdings.

Portfolio Turnover is important in a fund or portfolios overall performance. The FT[5] reports that the 20 funds with the highest Portfolio Turnover returned an average of just 4.7% over the 3 years to February 2011. Over the same period the 20 funds with the lowest Portfolio Turnover returned 16.8%! So not only are you paying more when your portfolio is churned, you maybe getting worse performance as well.

The long established principles of money management mean that there shouldn’t be a need for high portfolio turnover. If you get the asset allocation right from the start, only modest rebalancing will be needed unless there is a drama in the market. Herein lies the contradiction; if your broker doesn’t appear to be doing much you might wonder what you are paying for. It may be that they are bone idle, it may be that they have set things up right from the start. If there seems to be lots of activity, you might think they are being diligent, when in fact they are overtrading. There do exist some types of funds (for example Fidelity Funds Network) that allow switching of investment at low or fixed cost. This might appear attractive at face value, but they have sometimes performed poorly and suffered from high other charges. Thus there is no easy answer.

If you have any kind of investment, be that funds, shares, bonds or just a pension, you need to find out what the Portfolio Turnover rate is, why it is this and work out how much it is costing you. Your Stockbroker or fund manager won't like it, but you could be significantly worse off if you don't demand to know.

Honestly Banking

Twitter: @honestlybanking

[1] The Financial Times, 1/4/2011. The hidden costs of Portfolio Turnover by Alice Ross

[2] The Investment Management Association, http://www.investmentfunds.org.uk/press-centre/articles/2011/april

[3] The Investment Management Association Jargon Buster, http://www.investmentfunds.org.uk/investor-centre/jargonbuster/p

[4] Investment Week, We must stop 'corrosive' stock churning, Dec 2010

[5] FT, Ibid

{kind=link}

0 comments:

Post a Comment